Invasion to Evasion: How the Russo-Ukrainian conflict ties in with Tax Evasion

The 24th of February 2022 marked the beginning of a dark chapter in the history of the European Continent, with the reigniting of the conflict between Russia and Ukraine after a lull following the unilateral annexation of the Crimea Peninsula. The actions of the former have motivated a strong, widespread opposition by the International Community, which has mobilised and cooperated intensely in order to support Ukraine and reprimand the aggressor. While there have been several measures of support channelled towards Ukraine, the Community seeks to dismantle Russia’s military efforts by imposing a large set of sanctions. Amongst these, there has been put a symbolical and mediatic emphasis on the penalties directed at Russian oligarchs. These are individuals who hold offices of great relevance in Russian society with deep ties to the current regime, exercising great influence in the country’s main economic sectors and governmental agencies. Regarding this matter, the approved sanctions involve seizing property (real estate, vehicles, yachts and other luxury possessions), freezing bank accounts and other financial assets and the prohibition of entering or procuring goods and services in an ever-growing number of jurisdictions.

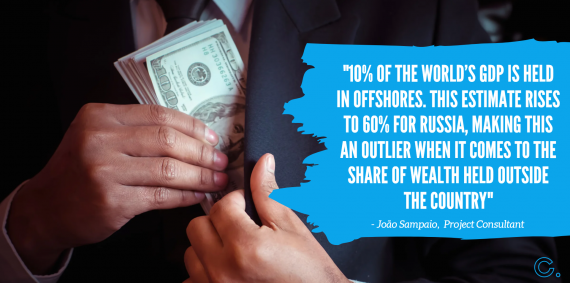

Several specialized analysts consider that about 10% of the world’s GDP is held in offshores. This estimate rises to 60% for Russia, making this an outlier when it comes to the share of wealth held outside the country. In fact, in 2008, Filip Novokmet, Thomas Piketty and Gabriel Zucman estimated that the amount of financial wealth owned by the wealthiest classes abroad surpassed the total amount of wealth reserved inside the country by the general Russian population. Therefore, at a glance, it would seem that Russia is particularly exposed to these kinds of measures, which the Community sought to exploit.

However, the effectiveness of these measures has been questioned, in light of the fact that they are not a new development. They had already been employed for a significant amount of time, albeit less vigorously. Intelligence Agencies around the world have uncovered that the Russian regime had warned its “partners” of incoming sanctions by the West months prior to the invasion. For the most brazen ones who did not heed the warning there are mechanisms in place to allow the most prosperous entities to obscure their wealth, particularly the portion which takes the form of financial assets (instead of physical assets, like the examples mentioned above), which is how most of the capital accumulated by the upper classes is retained.

In fact, there exists a whole industry dedicated to cloaking the real beneficiaries of these securities. As described by Gabriel Zucman in his book “The Hidden Wealth of Nations: The Scourge of Tax Havens”, tax havens are countries which commercialise their sovereignty by offering highly favourable tax regimes to encourage companies and individuals to underhandedly transfer their profits and wealth towards their jurisdictions. By unfairly competing with their counterparts, these States collect huge sums in taxes that they would not otherwise.

The targeting of these individuals/groups, a promising alternative to sanctions that impoverish the population as a whole (which, historically, has had undesired consequences), is, therefore, hindered due to our lack of knowledge about their real financial wealth. In this context, Zucman has stated that his proposal to consolidate, expand and bridge national registers to create a global financial register would allow authorities to unveil and strike at this hidden wealth (and consequently the upper classes, who have benefited the most from the regime) in a more comprehensive way, making the sanctions more successful. Organisations such as the International Centre for Tax and Development (ICTD) and the Independent Commission for the Reform of International Corporate Taxation (ICRICT) are attempting to make the most out of the situation by pushing decision-makers to bring about breakthroughs in this matter.

The responses to recent crisis have put tremendous strains on the budgets of States across the globe, many of which were already highly indebted. In the most severe cases, resorting to international institutions for aid, such as the IMF or the World Bank, entails the adoption of regressive austerity measures (such as the increase in food and fuel taxes or public expenditure cuts). Numerous recipients of these relief loans are underdeveloped countries facing serious humanitarian crisis, while underhanded expatriations of capital remain prevalent.

Inevitably, these countries must secure sufficient tax revenue. Honing in on the poorest cohorts of the population (reliant on labour income and less able to evade taxes) might not be sustainable, given that they may not be able to support (or even tolerate) high tax burdens in the midst of economic recessions, inflation and unemployment. Even if we don’t agree with the proposals formulated until now (like the European Commission’s CCCTB mechanism for the allocation of multinationals’ profits), it is evident that we must achieve a new tax paradigm prioritising transparency and equality.